UK Retail Media Decoded: Where Amazon, Boots, and Tesco Stand in 2026

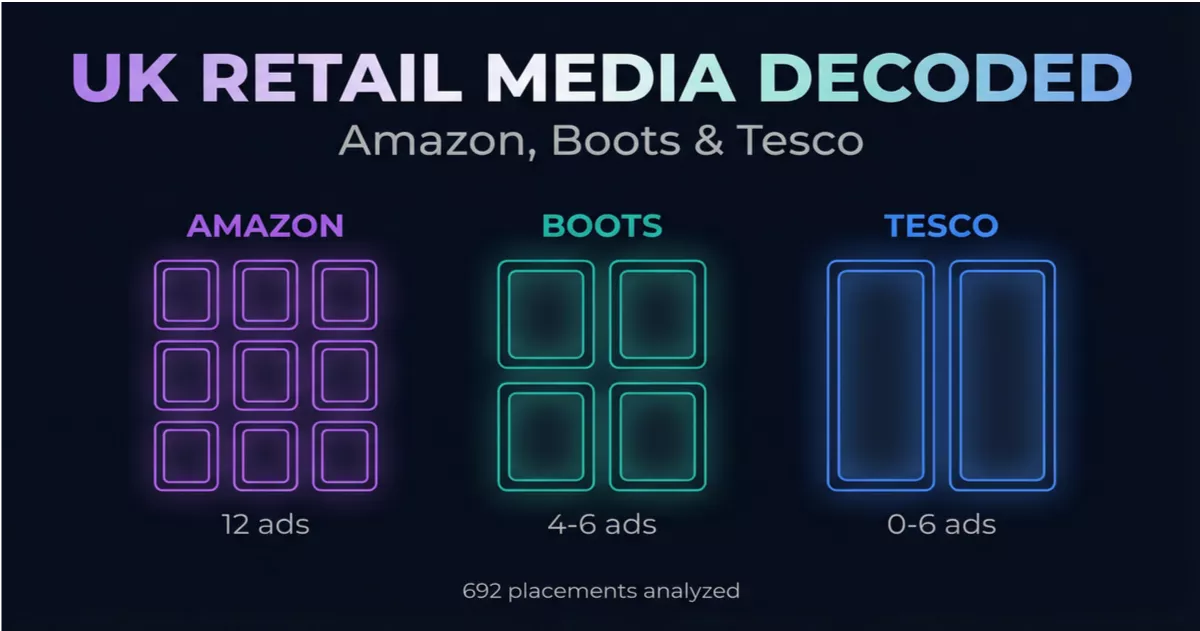

A comprehensive analysis of 692 sponsored placements across 31 keywords reveals the three-speed market shaping UK e-commerce advertising

We analyzed 31 high-intent keywords across Health & Wellness, Beauty & Skincare, and Medicine/OTC categories on three major UK retailers. The result? A clear picture of a market operating at three distinct speeds—and significant whitespace for brands willing to move strategically.

The Three-Speed Market

The UK retail media landscape is not a level playing field. Our analysis of 692 sponsored product placements reveals three retailers operating at fundamentally different levels of maturity, competition, and monetization.

Platform 1: Amazon — The Saturated Giant

Amazon.co.uk is the most mature and competitive retail media environment in the UK. Every single keyword we analyzed returned the maximum 12 sponsored products, alongside 2-3 brand display banners and 1-2 video ads. Ad density runs at approximately 20% of all visible product cards.

The platform is dominated by DTC brands and native Amazon sellers. Nutravita and WeightWorld appear across 6+ keywords each, leveraging the full ad format mix (Sponsored Products, Brand Banners, and Video). Traditional CPG brands like P&G and L'Oréal compete here but face significantly higher competition than on other UK retailers.

The Amazon Reality: This is a pay-to-play environment where organic visibility is minimal. Brands must invest heavily in Sponsored Products just to maintain category presence. The upside? Amazon offers the richest ad format mix of any UK retailer, including Sponsored Brand Video—a format unavailable on Boots or Tesco.

Platform 2: Boots — The Premium Middle Ground

Boots occupies the middle ground with moderate sponsored product density (typically 4 per keyword) but differentiates through premium display advertising. We observed brand display banners on 18 of 31 keywords—large hero units with 'SHOP NOW' CTAs that sit above all product results.

The platform is dominated by L'Oréal Group (CeraVe, La Roche-Posay, Garnier) and P&G (Pampers, Oral-B), both of which run coordinated multi-brand campaigns across Sponsored Products and Display. Boots also offers a unique 'SPONSORED' inline banner format observed for Pampers, Philips, and La Roche-Posay.

Whitespace Opportunity

12 of the 31 audited keywords had no brand display banner on Boots. These premium hero placements deliver massive visibility—and they're available on keywords including vitamin C, protein powder, collagen powder, mask, vitamin serum, and menopause supplements.

Platform 3: Tesco — The Under-Monetised Opportunity

Tesco's retail media network is significantly under-monetised compared to Amazon and Boots. 9 of 31 keywords (29%) returned zero sponsored products. Maximum sponsored density is just 6 per keyword, compared to Amazon's 12 and Boots' 8.

The platform shows extreme brand monopoly patterns. When brands advertise on Tesco, they frequently own every available slot:

- Aveeno holds all 6 moisturiser positions

- NIVEA holds all 6 sunscreen positions

- Benylin holds all 6 cough syrup positions

- Pampers monopolises all 3 nappies slots

- Oral-B owns all 3 electric toothbrush slots

This pattern suggests low competition for Tesco media inventory. The platform is dominated by large CPG brands (P&G, NIVEA, Aveeno, J&J), leaving significant whitespace for challenger brands, DTC players, and prestige beauty.

The Tesco Whitespace: Niche health keywords like magnesium, iron tablets, zinc supplements, collagen powder, and menopause supplements all returned zero sponsored products. Any brand activating Tesco retail media on these terms would have 100% share of voice with zero competition.

Tesco's Display Banner Expansion

Tesco is beginning to offer display banners—a significant development. We observed the first Tesco brand display banner on 'ibuprofen' (Nurofen's 'TOGETHER, LET'S CLOSE THE GENDER PAIN GAP' campaign). This suggests the platform is expanding ad formats beyond Sponsored Products, creating an early-mover opportunity for brands that engage Tesco media sales now.

The Big Spenders: P&G and L'Oréal

Two advertisers stand out for their aggressive, multi-retailer campaigns:

P&G (via Spark Foundry)

P&G is running coordinated campaigns across all three retailers. Pampers dominated 4 Sponsored Product positions on Boots 'nappies', all 3 positions on Tesco, and all organic positions on Amazon. Oral-B held Position 1 on both Boots and Amazon 'electric toothbrush', and all 3 slots on Tesco.

L'Oréal Group

L'Oréal is the most visible advertiser on Boots, with 9+ brands (CeraVe, La Roche-Posay, Garnier, L'Oréal Elvive) running across 8+ keywords via both Sponsored Products and Display. On Amazon, Lancôme held all 4 top slots for 'face cream' alongside a Brand Banner.

Platform Comparison: Ad Formats

| Ad Format | Boots.com | Amazon.co.uk | Tesco.com |

|---|---|---|---|

| Sponsored Products | Yes (4-8 per KW) | Yes (12 per KW) | Yes (0-6 per KW) |

| Brand Display Banner | Yes (18/31 KWs) | Yes (most KWs) | Yes (1 KW: ibuprofen) |

| Sponsored Video | No | Yes (1-2 per KW) | No |

| SPONSORED Banner | Yes (3 KWs) | N/A | N/A |

Strategic Whitespace Opportunities

1. Tesco Niche Health Keywords Are Wide Open

Magnesium, iron tablets, zinc supplements, collagen powder, and menopause supplements all returned zero sponsored products on Tesco. These are high-margin, health-focused searches with meaningful purchase volumes. Any brand activating Tesco retail media on these terms would have 100% share of voice.

2. Tesco Beauty Has Low Competition Outside CPG Giants

Foundation, mascara, and vitamin serum returned zero sponsored products on Tesco. The platform's beauty advertising is dominated by a handful of CPG brands (NIVEA, Aveeno, Garnier), leaving significant whitespace for prestige, DTC, and challenger beauty brands.

3. Amazon Video Ads Create Differentiation Opportunity

Amazon is the only UK retailer offering sponsored video ads in search results. SURI ran a Sponsored Brand Video on 'electric toothbrush' that played automatically in the results grid. Brands with strong video content (product demonstrations, ingredient stories, before/after) can stand out dramatically against competitors using static product listings.

4. Cross-Platform Presence Is Rare

Very few brands advertise consistently across all three retailers. L'Oréal Group and P&G come closest (multi-brand, multi-retailer). Most brands focus on a single platform. A coordinated cross-retailer media strategy could deliver significantly higher category share of voice than competitors who advertise on only one platform.

The Takeaway: Match Your Strategy to Platform Maturity

The UK retail media landscape requires a differentiated approach by platform:

Amazon: This is a high-investment, high-competition environment. Success requires aggressive bidding, full ad format utilization (including video), and continuous optimization. Organic visibility is minimal—you must pay to play.

Boots: The premium middle ground. Moderate competition on Sponsored Products, but significant opportunity in display advertising. Brands should prioritize securing hero banner placements on high-intent keywords where competition is still low.

Tesco: The under-monetised opportunity. Low competition, frequent monopoly positions, and significant whitespace on niche health and beauty keywords. Brands that move now can secure dominant share of voice before the platform matures.

The brands winning across all three platforms—P&G and L'Oréal—are running coordinated, multi-retailer campaigns. They understand that UK retail media is not a single market, but three distinct environments requiring three distinct strategies.

Methodology: This analysis is based on automated browser scraping of live retailer websites during the week of 24 February 2026. We recorded every product card marked 'Sponsored' by the retailer, every brand display banner, and every video ad unit across 31 keywords. All data reflects a single point-in-time snapshot. Sponsored placements change based on bidding dynamics, time of day, budget pacing, and A/B testing. Results may differ on repeat visits.

.png)